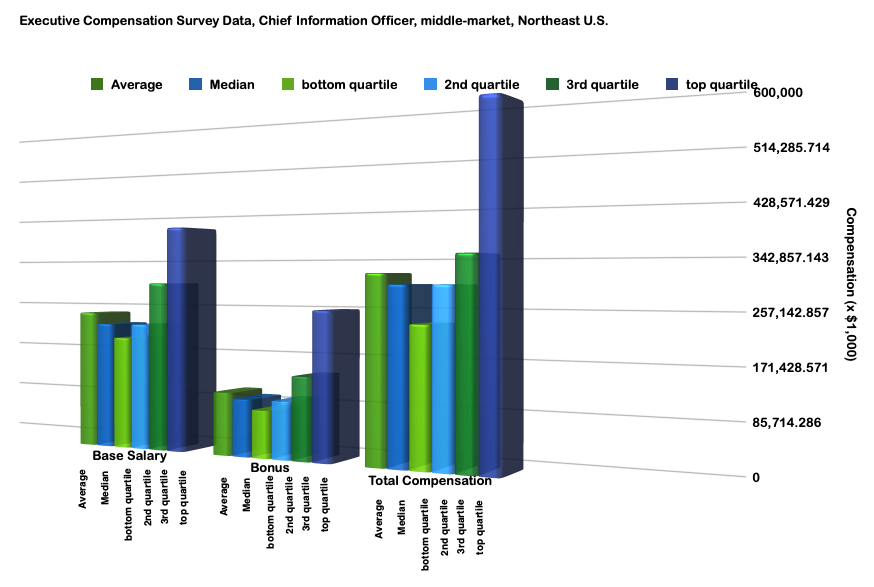

Executive Compensation Survey: Chief Information Officer, Manufacturing, Northeast

A recently completed search for a Chief Information Officer (CIO) role for a Northeast-based manufacturing ...

Read More